Reinstating Profitable Production Rights, Part I

Introduction

People, Ideas & Objects are reinstating a modified Profitable Production Rights Licensing method of generating the necessary revenue for the development of the Preliminary Specification and our user community. Providing Profitable Production Rights Licensees with the unique opportunity to participate simultaneously in both the North American oil & gas industry and its ERP software markets. All businesses in the 21st century will soon be software businesses. On March 15, 2022 we suspended our Production Rights initiative to pursue what we were calling our “Marshall Plan.” A means in which producers could deal directly with the issues in the industry as a result of it being elevated to the level of a political weapon in the form of the ongoing European crisis. To which producer officers and directors applied their “muddle through” strategy. The confusion and lack of coherence in the global oil & gas marketplace is evidence that all is not as it seems.

I’ve made a number of changes to the Profitable Production Rights License and better defined the opportunities for all concerned. It is a means in which the development of the Preliminary Specification can be undertaken and for licensees to hold the rights to control who will have access to People, Ideas & Objects software and our user communities service provider services in the form of our Cloud Administration & Accounting for Oil & Gas. I’ll restate here why participation in People, Ideas & Objects et al is valuable in the 21st century.

It’s no longer enough to just own the oil & gas asset, it’s also necessary to have access to the ERP software and services of People, Ideas & Objects et al’s Cloud Administration & Accounting for Oil & Gas that makes all oil & gas assets profitable.

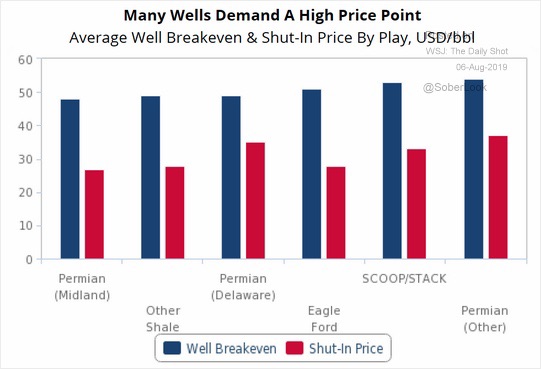

Oil & gas producer officers and directors have proven they don’t have an interest in oil & gas in their transitions to clean energy and their declaration that shale will never be commercial. A capitulation of the oil & gas business that others were responsible for building. Officers and directors have proven they don't have an understanding of, need or how to go about earning “real” profitability over these past four decades. Oil & gas producers have proven to hold a legacy and culture that is incapable of change and one that is counter to profitability and productivity. The first step in changing a culture is accepting there’s an issue. The key issue being chronic and systemic overproduction, or unprofitable production, such as natural gas is experiencing today. An issue People, Ideas & Objects et al resolves. An issue we see today in natural gas. Oil & gas producer officers and directors are not interested in being transparent in their accountability through their proven specious accounting methods and reporting, ad hoc ERP systems and dysfunctional organizations.

At this point in time what more needs to be proven that the North American producer is a failed organization? How many more chances will they be provided with? Societal jeopardy is now in play with what I perceive is the industry's inability, over the next decade, to maintain the volumes of shale’s deliverables over the mid to long term. For example U.S. natural gas production from shale is almost 80% of its total production. With 10,000 to 25,000 man hours of mechanical labor contained within each barrel of oil equivalent, the producers officers and directors self-interest overrides all other concerns. With all that has happened between producers and their investors since 2015. With the well defined expectations of their investors. It’s difficult for me to comprehend how they can explain their desire not to invest in enhanced profitability.

I came across this statement regarding what is defined as the Fifth Estate.

The Fifth Estate is a fundamentally different kind of power. It’s more difficult to consolidate than media, and more difficult to control than even our government divided by design. Its impact is also far more difficult to predict. This is because technology is above all things defined in terms of newness, which not only makes it disruptive of pre-existing power, but destructive of itself -- a sort of anti-power that only guarantees change. The true failsafe. Our ultimate reset. Tremendously empowering of tyranny in times of stagnation, technology is also our most powerful weapon against tyranny in times of innovation.

- Edmund Burke

We’ve lived through an interesting period where a transition has been taking place in the business community. One that has seen new Information Technology driven business models disintermediate the old with new, highly productive and value generating methods of conducting business. Over the past two decades the status quo has maintained control while everything in their business became distorted and value effectively destroyed. Since the 2008 financial crisis we’ve witnessed shale technologies become dominant however little to no value has been realized as a result. I see this period as the last of the “tremendously empowering of tyranny in times of stagnation.”

The oil & gas industry is not only faced with its most challenging operational, financial and political future. These three challenges demand that innovation, entrepreneurship and the principles that have brought the North American continent to dominate the global economy be put forward to resolve the industry's difficulties. The status quo is not only incapable, it has chosen not to bother, shrugged its shoulders and moved on. It is therefore a time when “technology is also our most powerful weapon against tyranny in times of innovation.” The choices we make today are how we’ll perform in 2025, 2030, 2040 and 2050.

It is People, Ideas & Objects opinion that the status quo has failed. Since 2015 they have unsupported capital structures. Have failed to act to remediate any aspect of these issues leading to their difficulties. Have deprecated their internal Work-in-Progress capabilities. Destroyed the service industries capital structures and the motivations for their people to seek employment there, capacities are operating at 40% of prior levels. And possibly most detrimentally of all, the leadership in the industry do not concern themselves with these concerns. Instead saunter off the stage into unrelated businesses involved in “clean energy.” Taking the oil & gas revenues in unauthorized fashion, that were generated by their investors and are the only source of financial capability available to fund the rebuild of this industry.

Producers are organizationally unprepared to approach their most challenging future and have not supported any method of organizational development. Leaving People, Ideas & Objects as the only alternative in the marketplace to this failed, archaic method. The only solution that has been researched and reviewed. Constructed on the basis of performance that provides for the most profitable means of oil & gas operations, everywhere and always. To build a dynamic, innovative, accountable and profitable oil & gas producer and industry to ensure that North America attains its optimal economic prosperity through energy independence by commercializing shale.

People, Ideas & Objects et al’s Profitable Production Rights Licensees own the keys that producers will need to access our Cloud Administration & Accounting for Oil & Gas method of profitable oil & gas organization. Or, producers could choose to remain with what usable life they have in the status quo, let that expire, and check to see what may be available then. In the meantime explain to their investors why they continue their unprofitable ways.

Profitable Production Rights License

The origins of our Profitable Production Rights Licenses were previously captured within a cryptocurrency or coin. We have deemed this to be unnecessary as the ability to lease these rights will be contractually managed within the Profitable Production Right Licensees control. The Coin was a distraction that may have tainted the prior method acceptability and with all that has happened in the crypto arena, I’ve realized that the coin was featureless for our purposes and redundant.

In terms of implementation, what we need is the ability to write each of the Profitable Production Rights Licenses into a blockchain solely dedicated to securing the Profitable Production Rights License. We thankfully are able to do that through Oracle Cloud Infrastructure and the use of their Oracle Autonomous Database’ recent development of the Oracle Blockchain Table as described below. This will be an Oracle database within the Preliminary Specification that manages these Profitable Production Rights Licenses by controlling producers' access to the software and services of People, Ideas & Objects et al and will manage the licensees revenue and expenses on their behalf.

Any assignments, sub-leases or transfers of the Profitable Production Right License do not override or delete the original purchaser's transaction in the database; they will write a new block on the chain, or row on the instance of the Oracle Blockchain database. Each Profitable Production Rights License is therefore aggregated through its serial number in order to determine all the associated transactions, assignments, its current ownership, and licensing of its production right to which producing Joint Operating Committee.

Ownership and control of the encryption Key to access the Profitable Production Rights record database will be held by the licensee of the Profitable Production Right. The contract they execute with the producer for the production will be maintained in this database and form the basis of the Profitable Production Rights Licensees billing to the producer. Where the licensee holds the access rights to what we believe will become the only means to profitably organize North American oil & gas exploration, production, administration and accounting. From Oracle.

A blockchain table is an append-only table designed for centralized blockchain applications.

In Oracle Blockchain Table, peers are database users who trust the database to maintain a tamper-resistant ledger. The ledger is implemented as a blockchain table, which is defined and managed by the application. Existing applications can protect against fraud without requiring a new infrastructure or programming model. Although transaction throughput is lower than for a standard table, performance for a blockchain table is better than for a decentralized blockchain.

A blockchain table is append-only because the only permitted DML are INSERT commands. The table disallows UPDATE, DELETE, MERGE, TRUNCATE, and direct-path loads. Database transactions can span blockchain tables and standard tables. For example, a single transaction can insert rows into a standard table and two different blockchain tables.

It should be noted that Oracle Blockchain Database is not a pure implementation of blockchain technology. It does not distribute a blockchain to other servers for validation and verification of the blockchain in the event of a suspicious transaction. It is focused on higher transaction based performance than the traditional blockchain technology is able to provide. A necessary requirement for our purposes. It is managed by the Oracle Autonomous Database and will act as a gatekeeper to our Cloud Administration & Accounting for Oil & Gas. In other words the data is immutable which is the feature of all blockchains. We are using it to ensure the Profitable Production Rights Licensees security of their rights. Each of the North American oil & gas producers will need to secure adequate Profitable Production Rights Licenses in order that their organization can access our Cloud Administration & Accounting for Oil & Gas software and service to obtain the most profitable means of oil & gas operations. People, Ideas & Objects believe that once constructed there will be no other competitive options in which producers can organize themselves profitably.

Flexible Profitable Production Rights License

Oil & gas production can be variable at times. Fields can and are susceptible to decline with shale being particularly variable. There is also the market demand as we’ve seen with an overall decline of 25% worldwide consumption during COVID. Although it is doubtful to happen again it forms a baseline. Add to this the variability that the Preliminary Specification is introducing with the decentralized production models price maker strategy. And production volume variability may become more significant and difficult to predict. How would this be manageable with the Profitable Production Rights License unable to earn revenues for at least a month or more, yet be obligated to cover the associated fixed overhead costs attributable to their license(s).

Therefore we are introducing two categories of Profitable Production Rights. What has been described to this point as one category. The second category will be assigned on the basis of 33.3% of the total amount of Profitable Production Rights License and be designated as Flexible Profitable Production Rights License. These will absorb the variability in production volumes up to the 33.3% level of all production on a priority basis. Whereas each producing property will automatically be assigned 33.3% of the Flexible Profitable Production Rights License to offset any production decline. Therefore the Flexible Profitable Production Rights License indemnifies the Profitable Production Rights License owners in case of variable production volumes up to the level of 33.3% of a Joint Operating Committee total production volume.

A Profitable Production Rights Licensee would therefore maintain their revenue streams in cases of production variability up to the extreme volumetric declines that we’ve seen in this past decade. As production is being shut-in due to the lack of profitability, this is anticipated to be a small percentage of the total output of North America. Therefore if the shut-in production is attributable to the lack of profitability and meets the following conditions.

Where the property is being actively reworked to be put back into production. The defined purpose of the Preliminary Specification.

Then the Flexible Profitable Production Rights License will assume those volumes as part of their overall allocation and absorb the revenue loss on any shut-in production of those properties on behalf of the Profitable Production Rights Licensee assigned to the property. Abandonment or suspension of the properties production would release all of the Profitable Production Right Licensees to seek new production elsewhere. Until such time as the production deliverability in North America dropped 33.3% below the base production volume established for the continent. Then there would be no effect on the Profitable Production Rights Licensees, only on the Flexible Profitable Production Rights License in terms of revenue loss.

The Flexible Profitable Production Rights License is not valued below the Profitable Production Rights License in terms of its purchase price when distributed. This is a result of the Flexible Profitable Production Rights License being fully acquired by myself. I am accepting 16.65% of the overall licenses, or half of the Flexible Profitable Production Rights License in consideration for 50.0% of the compensation of my 33.3% Intellectual Property royalty portion of the Preliminary Specifications budget. The other half of the Flexible Profitable Production Rights License is in consideration for the same percentage values of the Profitability of People, Ideas & Objects. What I expect as a result of holding all of the Flexible Profitable Production Rights Licenses is to have a strong negotiating position when leasing these to the producer firms that need to secure Flexible Profitable Production Rights Licenses on one third of all their production. In the interests of transparency and accountability, I am committing to publish the communications and negotiations that I have with producer firms regarding their securing the Flexible Profitable Production Rights they need for their production.

What do the Flexible and Profitable Production Right License earn?

Flexible and Profitable Production Rights Licensees are the exclusive customers of People, Ideas & Objects Preliminary Specification and our user communities service provider organizations. There will be no ability to access the Cloud Administration & Accounting for Oil & Gas software and services they’re building without the associated Profitable Production Right License in place to do so. What each individual Profitable Production Right enables is the means in which to process one barrel of oil equivalent / day in a profitable manner through this facility. Please note there will be an unknown period of time during development in which no revenues will be earned and no expenses incurred by either class of the Profitable Production Rights Licensees. This would not preclude the licensees from engaging the producers to ensure they have their production rights in place prior to commercial release. Profitable Production Rights Licensees revenues are earned by charging producers access fees to profitably process their boe on a monthly basis through the Cloud Administration & Accounting for Oil & Gas software and services. How those are structured will be an interesting development as we proceed.

Producers methods today have failed, have destroyed what value had existed in the industry prior to their administration and the subsequent investments made. They have not generated any value from the massive call on investors and are incapable of dealing with today’s issues and opportunities. Oil & gas producers have proven to be incapable of managing the business and are in fact failed organizations with capital structures that are unsupported. Officers and directors today are managing a capital intensive industry with reasonable cash flows that are only capable of providing for their executive compensation. There has been and will be no change from this during their tenure. It is within that statement that the value of the Profitable Production Rights can be discerned. What is the difference between a truly profitable oil & gas operation and the one that has been carried out in the industry since the initial 1986 oil price collapse? Where the North American oil & gas industry would be capable of performing against all other industries for capital. That is the value that the Profitable Production Right Licensees offer the producer firm. It is within this People, Ideas & Objects value proposition that the Profitable Production Right Licensees are leveraging their revenue stream. The exclusive right to grant the dynamic, innovative, accountable and profitable oil & gas producer the ability to organize, operate and provide for the most profitable means of oil & gas production. The methods and means of operations are described in the Preliminary Specification and cover the full scope of exploration, production, administration and accounting for the start-up to integrated producers.

Although the producers have not listened to their investors and bankers demands to accommodate their needs. It will be interesting to see the producers' argument why they’re not participating in the Profitable Production Rights Licenses for the production they have. Why are they so committed to unprofitable production or is clean energy really that attractive?