Price Maker vs. Price Taker, Part II

On Monday we mentioned we’d be discussing the concept of production discipline that the Preliminary Specification brings about. The price maker strategy is valid only when the producers adhere to the simple business principles of ensuring that there is an accurate costing of the oil and gas produced. That unprofitable properties are shut-in within the first month or two of their being determined to be unprofitable based on that accurate and detailed accounting information. And some form of production discipline is instituted across the North American industry and this is enforced reliably, consistently and fairly. People, Ideas & Objects have chosen profitability as it is the only fair and reasonable method of production allocation. Government mandates and OPEC allocations based on reserves are unable to be applied fairly when political influence is asserted. These are the three requirements that make the price maker strategy of our decentralized production model operational in the Preliminary Specification. They are sound in theory, however in practice we have seen throughout the industry, and most particularly the history of OPEC in the 1980’s and 1990’s when they had substantial surplus capacity. The ability to maintain quotas, or some form of production discipline in oil and gas is very difficult. The need for cash creates the issue, it therefore motivates cheating and production discipline is easy to overcome when oil and gas commodities are fungible.

It is in that sense that the Preliminary Specification appears to provide the incentive for cheating when the return of the cash incurred as overhead is returned the subsequent month as one of its primary advantages. This is immediately provided to the oil and gas producer as we noted in Monday’s post. The ability to also extract the previously invested cash for reuse as capital expenditures, to pay dividends or reduce debt is the effective way in which the industry will provide a prosperous and profitable operation throughout its next three decades. However, getting the full value of the oil and gas resources as they’re represented in the reserves in place needs to be achieved in order to fulfill the objective of maximizing shareholder value. Let’s have a look at these three requirements in detail and understand how the production discipline of the Preliminary Specification is implemented.

An accurate costing of the properties oil and gas commodity costs needs to be rethought as the principle of unlimited capital provided by banks and investors was only viable when they were deceived. In the real world deferral of all costs to property, plant and equipment, then to deplete these over decades doesn’t make sense in a commercial environment. The SEC dictates the accounting for the costs of capital will not exceed the value of the reserves of the producer. The producers have interpreted that to mean that the objective of the firm is to raise the value of property, plant and equipment to what the value of their reserves are. Which is ludicrous. The competitive producer will seek to turn over their capital costs in order to recover the cash invested for its reuse. If this extinguishes property, plant and equipment then that is an operation that will be hard to outperform from a competitive point of view. As we noted on Monday the direct charges of overhead to the Joint Operating Committee, as opposed to being capitalized in property, plant and equipment, is an attribute of the Preliminary Specifications decentralized production models price maker strategy. When the actual costs of oil and gas exploration and production are being accounted for then we can begin to account for the properties that are providing benefit to the firm, profitable, and those that are not, losses. Currently in oil and gas the ability to discern which property is actually profitable is about as easy as separating the ingredients of fudge. It cannot be done.

There are regulations for the type of accounting that is undertaken by the oil and gas producers. Regulations that are dictated by not only the SEC but also other regulatory bodies such as royalty, tax… The amount of leeway and interpretation of these regulations within the industry is not a feature of the creativity of the accounting staff, more to do with the quality and experience of the staff that the producer employs. The major integrated producers have policies and procedures that are very sophisticated and are fundamentally different than what a small producer may employ in the process of “getting the quarter out.” Nonetheless all are within the requirements of those regulations. The sophistication is the determining factor. The Preliminary Specifications service providers introduce a new level of standardization of oil and gas accounting. Whether a startup or integrated major the need to meet these regulations is necessary and that will continue. However, when the accounting for recording the butane sales of a property is conducted by the appropriate service provider, that will be calculated in the manner in which our user community, the principle of the service providers organization, and the industry representatives determine they want that process managed. And the management of that process will be the same for all producers and the costs of managing that process will be the same for all concerned. The need for startup producers to have hundreds of thousands of dollars of administrative and accounting staff to conduct their accounting and administration will be reduced to the incidental fees that the service providers charge for the actual work that was completed and necessary. If there were no profitable properties producing, the startup oil and gas producer would not be incurring any of these costs. There are also distinct advantages for all the producers in the industry for a standardized methodology of administrative and accounting overhead costs. Particularly when these costs are shared across the producers who are involved in the Joint Operating Committee. Having a standardized accounting of these costs prepared by three thousand independent service provider organizations working on behalf of the entire industry ensures that no one is being treated unfairly.

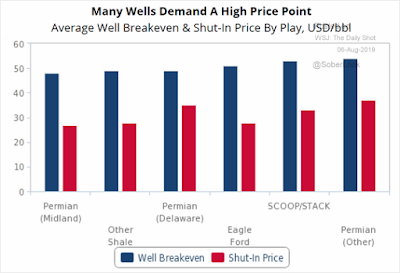

The following graph has been used in the White Paper and shows exactly how oil and gas has become the financial armageddon that it currently is. Source @SoberLook

Note this graph reflects that Well Break Even and Shut-in prices denote that at any point, and as long as the commodity price covered the operating costs, the property would continue to produce regardless of the impact on capital costs. If a dollar of capital costs was being returned, or one dollar above the shut-in price, that would enable the production of the property to continue. Only at the point in time where the commodity price dropped below the operating costs would the producer allegedly shut-in their production. This is a fundamental misinterpretation of the term break even, it is the reason the industry is in the difficulty that it’s in and why the producers have continued to lose money for the past four decades. Break even is not what is being interpreted here. What in fact the producer is assuming is that as long as there is cash flow above the operating costs then they’re making money and will continue to produce. What they’re stating is acceptable is they may not be breaking even, but they’re generating cash flow.

What People, Ideas & Objects provide in our Preliminary Specification, if we could assume the accuracy of this graphs numbers, is the point at which the property would be shut-in would be at the breakeven point and below. The reason for this being the production discipline gained through knowing that producing any property unprofitably only dilutes the producers corporate profits. Producing below the breakeven point is the point where unprofitability begins. Producing below the breakeven point for one producer, in an industry who’s commodities are price makers, will have the effect where the price of the commodities will be dropped below the breakeven price for all producers. When all producers continue to produce below the breakeven price for four decades you have an exhaustion of the value from the industry on an annual and wholesale basis. Times were only “good” when investors were willing.

You hear investors demand that producers begin to return more of their invested capital. Investors are always the most efficient communicators. If only producers would listen. If a property does not produce a profit, above the breakeven point in this graph, then it has to be shut-in. Which is the production discipline we’re talking about, which leaves nothing to say about the discipline portion of the claim. If a producer continues to produce properties unprofitably then the only ones they’re fooling are themselves. Their profits are being diluted by these unprofitable properties in two material ways. First these losses are offsetting their profitable property profits and therefore reducing the corporate profits earned. Secondly they are reducing the prices of the commodities by continuing to overproduce unprofitable production which as price makers, has a material effect on the price of the commodities their profitable properties receive.

To stand out as a high performing oil and gas producer -- it’ll be interesting to see if that becomes an overall corporate objective in oil and gas. Producers will need to fulfill their corporate objective to their shareholders. Maximize shareholder value. By maximizing profitability they will also maximize the value of their firms. Pretty simple really. But in that we have the inherent, implied discipline that would rule the North American producers in terms of why they’d adhere to the production discipline in the Preliminary Specification. I don’t expect the current bunch to make this transition, I’m on the record as saying they’re terminal, we are using disintermediation and creative destruction to shorten their usable, miserable lives. The corporate objective of profitability has other benefits that we’ll talk about on Friday, and why everyone, not just shareholders should be interested and motivated by this one simple corporate objective.

Throughout this Price Maker vs. Price Taker series I’ll be recreating the following graph which spells out one thing. Oil and gas commodities are price makers. Source @SoberLook

Any arguments on that point are now moot, in my opinion.

The Preliminary Specification, our user community and service providers provide for a dynamic, innovative, accountable and profitable oil and gas industry with the most profitable means of oil and gas operations. Setting the foundation for profitable North American energy independence. People, Ideas & Objects have published a white paper “Profitable, North American Energy Independence -- Through the Commercialization of Shale.” that captures the vision of the Preliminary Specification and our actions. Users are welcome to join me here. Together we can begin to meet the future demands for energy. And don’t forget to join our network on Twitter @piobiz anyone can contact me at 403-200-2302 or email here.

It is in that sense that the Preliminary Specification appears to provide the incentive for cheating when the return of the cash incurred as overhead is returned the subsequent month as one of its primary advantages. This is immediately provided to the oil and gas producer as we noted in Monday’s post. The ability to also extract the previously invested cash for reuse as capital expenditures, to pay dividends or reduce debt is the effective way in which the industry will provide a prosperous and profitable operation throughout its next three decades. However, getting the full value of the oil and gas resources as they’re represented in the reserves in place needs to be achieved in order to fulfill the objective of maximizing shareholder value. Let’s have a look at these three requirements in detail and understand how the production discipline of the Preliminary Specification is implemented.

An accurate costing of the properties oil and gas commodity costs needs to be rethought as the principle of unlimited capital provided by banks and investors was only viable when they were deceived. In the real world deferral of all costs to property, plant and equipment, then to deplete these over decades doesn’t make sense in a commercial environment. The SEC dictates the accounting for the costs of capital will not exceed the value of the reserves of the producer. The producers have interpreted that to mean that the objective of the firm is to raise the value of property, plant and equipment to what the value of their reserves are. Which is ludicrous. The competitive producer will seek to turn over their capital costs in order to recover the cash invested for its reuse. If this extinguishes property, plant and equipment then that is an operation that will be hard to outperform from a competitive point of view. As we noted on Monday the direct charges of overhead to the Joint Operating Committee, as opposed to being capitalized in property, plant and equipment, is an attribute of the Preliminary Specifications decentralized production models price maker strategy. When the actual costs of oil and gas exploration and production are being accounted for then we can begin to account for the properties that are providing benefit to the firm, profitable, and those that are not, losses. Currently in oil and gas the ability to discern which property is actually profitable is about as easy as separating the ingredients of fudge. It cannot be done.

There are regulations for the type of accounting that is undertaken by the oil and gas producers. Regulations that are dictated by not only the SEC but also other regulatory bodies such as royalty, tax… The amount of leeway and interpretation of these regulations within the industry is not a feature of the creativity of the accounting staff, more to do with the quality and experience of the staff that the producer employs. The major integrated producers have policies and procedures that are very sophisticated and are fundamentally different than what a small producer may employ in the process of “getting the quarter out.” Nonetheless all are within the requirements of those regulations. The sophistication is the determining factor. The Preliminary Specifications service providers introduce a new level of standardization of oil and gas accounting. Whether a startup or integrated major the need to meet these regulations is necessary and that will continue. However, when the accounting for recording the butane sales of a property is conducted by the appropriate service provider, that will be calculated in the manner in which our user community, the principle of the service providers organization, and the industry representatives determine they want that process managed. And the management of that process will be the same for all producers and the costs of managing that process will be the same for all concerned. The need for startup producers to have hundreds of thousands of dollars of administrative and accounting staff to conduct their accounting and administration will be reduced to the incidental fees that the service providers charge for the actual work that was completed and necessary. If there were no profitable properties producing, the startup oil and gas producer would not be incurring any of these costs. There are also distinct advantages for all the producers in the industry for a standardized methodology of administrative and accounting overhead costs. Particularly when these costs are shared across the producers who are involved in the Joint Operating Committee. Having a standardized accounting of these costs prepared by three thousand independent service provider organizations working on behalf of the entire industry ensures that no one is being treated unfairly.

The following graph has been used in the White Paper and shows exactly how oil and gas has become the financial armageddon that it currently is. Source @SoberLook

Note this graph reflects that Well Break Even and Shut-in prices denote that at any point, and as long as the commodity price covered the operating costs, the property would continue to produce regardless of the impact on capital costs. If a dollar of capital costs was being returned, or one dollar above the shut-in price, that would enable the production of the property to continue. Only at the point in time where the commodity price dropped below the operating costs would the producer allegedly shut-in their production. This is a fundamental misinterpretation of the term break even, it is the reason the industry is in the difficulty that it’s in and why the producers have continued to lose money for the past four decades. Break even is not what is being interpreted here. What in fact the producer is assuming is that as long as there is cash flow above the operating costs then they’re making money and will continue to produce. What they’re stating is acceptable is they may not be breaking even, but they’re generating cash flow.

What People, Ideas & Objects provide in our Preliminary Specification, if we could assume the accuracy of this graphs numbers, is the point at which the property would be shut-in would be at the breakeven point and below. The reason for this being the production discipline gained through knowing that producing any property unprofitably only dilutes the producers corporate profits. Producing below the breakeven point is the point where unprofitability begins. Producing below the breakeven point for one producer, in an industry who’s commodities are price makers, will have the effect where the price of the commodities will be dropped below the breakeven price for all producers. When all producers continue to produce below the breakeven price for four decades you have an exhaustion of the value from the industry on an annual and wholesale basis. Times were only “good” when investors were willing.

You hear investors demand that producers begin to return more of their invested capital. Investors are always the most efficient communicators. If only producers would listen. If a property does not produce a profit, above the breakeven point in this graph, then it has to be shut-in. Which is the production discipline we’re talking about, which leaves nothing to say about the discipline portion of the claim. If a producer continues to produce properties unprofitably then the only ones they’re fooling are themselves. Their profits are being diluted by these unprofitable properties in two material ways. First these losses are offsetting their profitable property profits and therefore reducing the corporate profits earned. Secondly they are reducing the prices of the commodities by continuing to overproduce unprofitable production which as price makers, has a material effect on the price of the commodities their profitable properties receive.

To stand out as a high performing oil and gas producer -- it’ll be interesting to see if that becomes an overall corporate objective in oil and gas. Producers will need to fulfill their corporate objective to their shareholders. Maximize shareholder value. By maximizing profitability they will also maximize the value of their firms. Pretty simple really. But in that we have the inherent, implied discipline that would rule the North American producers in terms of why they’d adhere to the production discipline in the Preliminary Specification. I don’t expect the current bunch to make this transition, I’m on the record as saying they’re terminal, we are using disintermediation and creative destruction to shorten their usable, miserable lives. The corporate objective of profitability has other benefits that we’ll talk about on Friday, and why everyone, not just shareholders should be interested and motivated by this one simple corporate objective.

Throughout this Price Maker vs. Price Taker series I’ll be recreating the following graph which spells out one thing. Oil and gas commodities are price makers. Source @SoberLook

Any arguments on that point are now moot, in my opinion.

The Preliminary Specification, our user community and service providers provide for a dynamic, innovative, accountable and profitable oil and gas industry with the most profitable means of oil and gas operations. Setting the foundation for profitable North American energy independence. People, Ideas & Objects have published a white paper “Profitable, North American Energy Independence -- Through the Commercialization of Shale.” that captures the vision of the Preliminary Specification and our actions. Users are welcome to join me here. Together we can begin to meet the future demands for energy. And don’t forget to join our network on Twitter @piobiz anyone can contact me at 403-200-2302 or email here.