These Are Not the Earnings We're Looking For, Part LXXI

Composition of Our Value Proposition

Tangible & Quantifiable Attributes

Profits

People, Ideas & Objects presents a solid value proposition, estimated to be between $25.7 trillion and $45.7 trillion over the next 25 years. This has been validated through the work we did in late 2023 to detail the revenue losses on natural gas incurred this century. The validation of this proposition comes from the deterioration of natural gas pricing structures over the years, which shifted from a heating value equivalent of 6:1 to as low as 50:1 by early 2024. These revenue losses, amounting to $4.1 trillion for the period from 2000 to 2023, have been portrayed by officers and directors as opportunity costs—a perspective we disagree with. The decline in natural gas prices stems from chronic and systemic overproduction. The Preliminary Specification we provide offers an ERP solution tailored for oil & gas producers to rehabilitate oil & natural gas markets. It’s clear that “muddling through” while oil & gas prices have deteriorated by over 800% in just two decades is simply unacceptable.

Our value proposition enhances overall oil & natural gas profitability through the implementation of the Preliminary Specification’s decentralized production model, projected to yield an additional $5.7 trillion over the next 25 years. The documented losses in natural gas reinforce the accuracy of our estimates concerning the impact of chronic overproduction. While we have quantified these natural gas losses based on observable price declines, objectively quantifying the revenue losses in oil has proven more challenging. Nevertheless, we believe our estimates are consistent with the historical trends observed over the past 23 years.

Our argument that oil & gas represent a primary industry seems to be overlooked by many officers and directors. However, we assert that much of the lost value also represents critical financial resources for the broader oil & gas economy. These losses affect not only producer profitability but also the essential resources needed by the service industry, including capital and operations for drilling and fracing fleets, and compensation to royalty holders for product title acquisition. The overall liquidity, functionality, prosperity, and profitability of the industry are at stake.

The responsibility to ensure the service industry remains vibrant and capable lies as much with producer officers and directors as it does with their own firms. The service industry is an extension of their firms, structured through markets to address the diversity of geographical regions and geological concerns. Without the market-driven solutions provided by the service industry, producer field costs would be exponentially higher, and the capacities and capabilities of the entire industry would face severe constraints. Rendering it far less productive.

Capital

The remaining $20 to $40 trillion of the quantifiable portion of our value proposition is derived from the innovative methods that People, Ideas & Objects employ to account for capital. These capital costs are essential for producers to build and sustain the oil & gas infrastructure and production across North America over the next 25 years. Our estimates are grounded in independently discussed capital expenditure projections within the market. Our value proposition hinges on the difference between the accounting method we advocate in the Preliminary Specification and the traditional practices that have dominated the industry for decades.

Currently, officers and directors operate under the belief that their role is to "build balance sheets" and "put cash in the ground." This approach involves capitalizing the majority of the producer's costs and depleting these over the life of the reserves, resulting in balance sheets that are excessively inflated and always inflating. When capital assets are overreported, it leads to the equal and inverse overreporting of profitability, which in turn attracts excessive investor interest for investment in the industry. This influx of investment contributes to further overproduction in oil & gas, leading to significant and ongoing price discounts, and occasionally, drastic price collapses—hallmarks of a market governed by the principles of price makers.

Their method is based on the flawed assumption that investors will cover capital costs, while consumers will bear operating expenses. However, since 2015, the withdrawal of investor capital has highlighted the industry's unsustainable reliance on external funding, revealing that genuine profitability is lacking. Despite our discussion and the evident issues, no significant changes have been made by officers and directors since 2015, leaving the industry in a state of peril.

In contrast, People, Ideas & Objects advocate for recognizing all capital within the first 30 months of a property's development—a method particularly relevant in the shale era, characterized by high costs, steep decline curves, and significant capital costs of rework. By recognizing capital costs over a shorter period, producers can pass these capital costs on to consumers, which is a reasonable expectation for a capital-intensive industry. Our value proposition aims to ensure that prior capital investments are returned to producers in the form of cash, enabling them to reinvest in further capital expenditures, pay dividends, and service debt. This approach eliminates the need for stock issuance or bank loans, except for substantial transactions. The continuous and iterative return of capital would provide producers with the financial resources needed to manage their operations effectively.

These attributes are the hallmark of a profitable firm. If producers seek more capital, they have the ability to generate it themselves by achieving genuine profitability. Despite my ongoing efforts over the years, producers have consistently refused to acknowledge that accounting plays a critical role in their performance. They often rely on the belief that only geologists or engineers can determine the profitability of a basin, as evidenced by statements like "shale will never be commercial" in 2021. This narrow perspective overlooks the complexities of business operations, focusing solely on the technical aspects while undervaluing the broader influence of accounting and business, which are often relegated to the simple task of paying the bills in producer firms.

Working Capital

When producers capitalize the majority of their costs, they include substantial portions of their overhead as capital. This practice results in the cash used for these monthly overhead expenses to not be replenished within the current period. Instead, the invested cash remains on the balance sheet for decades in some cases, forcing producers to seek new sources of cash each month to cover their recurring overheads. Essentially, producers fail to maintain what is commonly referred to in business as a "cash float." Over the course of a year, working capital is drained through capital expenditures and associated overhead costs. Since 2015, when investors ceased providing further capital support, the working capital within the industry has reached critically low levels. In response, officers and directors have resorted to extreme measures to sustain their capital expenditures, including delaying payments to the service industry for 18 months or more. This approach severely undermined the financial stability of the service industry, leading to a significant downturn, exacerbated by the subsequent COVID-19 lockdowns and then reduced activity levels among producers.

Producers must recognize that they operate within a primary industry, and their working capital should be viewed as a reflection of the financial health of the broader oil & gas economy. When producers mismanage their cash flow, they not only worsen economic downturns but also find themselves ill-prepared to take advantage of upturns or maximize opportunities. This situation arises because no one in the industry has sufficient cash to conduct the necessary level of business. The reliance on investors to meet the industry's cash needs is a phenomenon that can be attributed to oil & gas officers and directors who lack a fundamental understanding of business. The working capital of producers should be regarded as akin to the Federal Reserve’s role in keeping the industry operational—similar to the importance of maintaining the right amount of oil in an engine’s crankcase. The balance between too much or too little working capital is crucial.

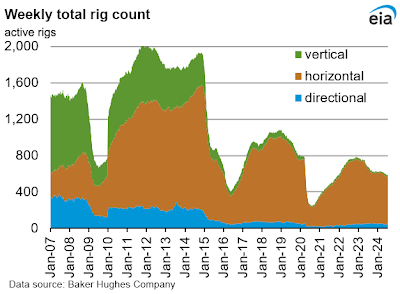

Producers serve as the Federal Reserve for the oil & gas economy. The correlation between the decline in active rigs, as shown by IEA data, and the exit of capital demonstrates that a healthy industry requires a greater volume of working capital within producer firms, which in turn supports the broader oil & gas economy.

Producers are currently unable to recover the majority of their costs in this capital-intensive primary industry. I have been discussing this issue for over a decade, yet nothing has been done to change the methods that exacerbate the problem. The lack of necessary cash within the system causes unnecessary stress throughout the broader oil & gas economy. Some argue that we should return to the gold standard to stabilize the value of the dollar, which is an impossibility. The dollar serves as a medium of exchange, not a store of value. Limiting the amount of money in the system constrains the volume of transactions that can occur. When cash is scarce, its value increases due to excess demand, but the economy suffers because fewer transactions can be undertaken. This scenario is akin to a vehicle with no fuel in the tank or oil in the crankcase, rendering it inoperable despite being mechanically sound.

By recognizing capital costs on an accelerated basis through the Preliminary Specification, producers and the industry as a whole can rehabilitate their working capital and cash flow issues. Officers and directors often believe that SEC requirements for full-cost accounting compel them to report the largest possible balance sheet, using the ceiling test as a target rather than the outer limit it is intended to be. In contrast, People, Ideas & Objects advocate that the most profitable producers would aim to reduce their property, plant, and equipment account balances to zero, reflecting that they have been profitable enough to retire all their incurred capital investments. Profitability, not cash flow, is the appropriate measure.

Cost Control

Controlling costs is a crucial endeavor for any organization, and it should be a top priority, especially since low-cost organizations tend to be more resilient. But what are the highest costs that oil & gas producers have been grappling with for decades? One of the most significant issues is the impact of unprofitable properties, which dilute the earnings of profitable ones. Producing reserves at a loss, particularly when prices are low or even negative, can be devastating to the prospects of financial recovery. For instance, if the cost of producing gas is $9 but it sells for only $3, the resulting $6 loss would require six profitable volumes sold at $10 just to break even. Such losses are highly destructive to earnings and diminish the reserve value of the producer—yet this reality seems to be beyond the comprehension of many current officers and directors.

Focusing on profitability is what truly generates value. When unprofitable production is shut in, it’s removed from the market, which increases overall revenues. By eliminating the dilution of profits from losing properties, the firm can report its highest possible profitability, no matter what its production profile may be. Unprofitable properties should be moved to the firm's inventory of innovation, where they can be returned to profitable production as soon as possible. This can be achieved through cost reduction, increasing reserves, boosting production throughput, or applying other innovative strategies. The goal is to use the firm's earth science and engineering capabilities to generate incremental profitability in the most innovative ways possible, finding the marginal price when only profitable production is maintained.

What many producer officers and directors fail to grasp is that these actions build incremental value. It’s true that no additional petroleum reserves may have been discovered or developed, but they’ve proven that reserves are essentially worthless if they can’t be produced profitably. This has been the case for decades, as the industry continues to consume cash in the process of production.

Alternatively, what would the present value of profitable shale reserves be? It’s here that we can find the limit of producers' business thinking. They believe that “building balance sheets” to a size that replicates the value of the reserves is the objective, for some reason. We discussed property, plant and equipment and the most profitable producers would have the lowest values recorded in that account. However, the reserves present value would soar based on the marginal price being realized and assessed against far greater volumes of the reassessed commercial reserves volume. Having “real” profitable operations however are not to be accepted. Recall the mid 1980s natural gas prices adjusted for inflation would today be about $10.00, not $2.14. Recall too that the mid 1980s was a time of 100% conventional production.

Alternatively, consider the present value of real or genuine profitable shale reserves. This is where the limitations of producers' business thinking become apparent. Many believe that the objective is to "build balance sheets" that mirror the value of the reserves, but this approach is misguided. We’ve already discussed that the most profitable producers would have the lowest values recorded in their property, plant, and equipment accounts. However, if they focus on achieving a marginal price that maximizes profitability, the present value of their reserves would soar, driven by far higher prices and greater volumes of commercial reserves. Returning the investors focus back on to reserves valuations. Yet, the concept of maintaining "real" profitable operations is rejected.

To put this into perspective, natural gas prices in the mid-1980s, when adjusted for inflation, would be around $10 today—compared to the current market price of $2.14. Shale has introduced new cost structures in the oil & gas industry; it has brought in initial or flush production volumes that have overwhelmed the natural gas price structure, driving it down from its heating value equivalent of 6:1 to as low as 50:1. This shift has had a devastating impact on the entire oil & gas economy. Devastating every source of value in every corner of the greater oil & gas economy.