The Opportunity

People, Ideas & Objects offers the Preliminary Specification for North American producers, providing them with the most profitable means of oil and gas operations, everywhere and always. A primary industry that previously relied on outside capital must now transition to become profitable enough to fuel its capital expenditures, investor dividends, and bank debt repayments. This industry transition is challenging at any time and place, demanding a cultural shift from “muddle through” complacency to a dynamic, innovative, accountable, and profitable model. Changing the culture to focus on preservation, performance, and profitability requires wholesale changes to rebuild the industry with that vision. Orchestrating such change internally would be futile and counterproductive. Change of this magnitude can only be successfully achieved through creative destruction, eliminating what no longer functions and replacing it with what will.

Thankfully, producer officers and directors have proven their culture is incapable of functioning any further and demands replacement. Objectively, the industry is beset by long-standing difficulties that have resulted in a protracted waste of inherent value. Producer officers and directors have failed to address the challenges they’ve placed on the greater oil and gas economy. The information contained within this graph from @Soberlook on X confirms what we suspected and supports our belief in the necessity of moving forward.

Who could blame the investors? For over four decades, officers and directors have used the industry to fuel what may become the greatest destruction of wealth and value known to mankind. Energy in the form of oil and gas is critical to our quality of life, economy, and survival. The documented destruction in this WorldOil article is just the beginning of the difficulties the industry will face.

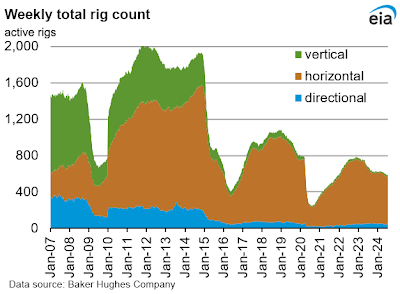

- The Permian basin is expected to join all other basins in experiencing production declines.

- 2023 saw 123 rigs dropped from the fleet and now stands at 654 rigs.

- (As of July 2, 2024 there are 585 rigs.)

- Drilling and Uncompleted Wells, or DUC’s have declined. As the WorldOil article states “the lower the count becomes, the longer it will take for shale supply to return.”

How is this happening? People, Ideas & Objects have clearly identified that it is the officers and directors, their “muddle through” mentality, well-built balance sheets, and other nonsense that have brought us to this point. Why has this happened? Not a penny of profit has been made by a single producer in the industry since the late 1970s. Nothing but the expenditure of investor money gained from specious accounting claiming oil and gas reserves were valuable. If they’re so valuable, why were they not produced profitably? What has been proven is that with willing investors, the useless spending machine of officers and directors will destroy any and all value.

Officers and directors used to proudly preach to me, "Who cares about profits? It's about cash flow.” They hardly understood why profits were necessary or that their talk about cash flow was ridiculous. Cash flow is nothing more than the return of capital invested. They never recognized that they were not profitable. With their always looming “ceiling test write-downs” proving they don’t even return all of the capital invested. They never understood what was needed to earn real profitability in a competitive market. What they have proven is they have no understanding, concern, or need to operate a profitable business. Since 2015, investors have given them ample time to figure out how to earn real profits. And what did they do? They declared shale unable to be commercial and moved on to clean energy, using oil and gas revenues to support their spending. If they want to pursue another industry, they should quit their jobs and pursue clean energy as a startup. What they did was at a minimum unethical.

In 2015, the Investors Acted

Outside of the media, merely claiming profitability does not make it true. Producer financial statements have been distorted to the point where they no longer represent performance through the accurate and timely recognition of costs. Instead, the objective has been to bloat balance sheets to approximate the value of the reserves. Given this context, a reevaluation of the industry is necessary to assess the "real" performance of producers. Overreported asset values have never sustained successful business models, achieving their success in ponzi schemes or fraudulent businesses, over the long term.

For the past nine years, no new investment money has flowed into oil and gas. Now, with a decade of inaction from producers to address profitability issues and the disaster documented in the WorldOil article, investors appear to be selling their positions and moving on. We see this as confirmation of People, Ideas & Objects' Preliminary Specification. Investors have lost patience with officers and directors and are leaving. The current outflow of funds is significant, and we expect this trend to continue for some time. This indicates the distaste that producer officers and directors are causing investors. Therefore, we believe now is an opportune time for the Preliminary Specification to move forward in our fundraising and software development activities.

These signals from oil and gas investors provide us with a clear understanding of the future. Our concern was that starting our software development without a clear signal from producer investors about their future actions could result in a terminally failed project. Such a failure would jeopardize our goal of rebuilding the North American oil and gas industry as proposed. We have represented our position to the investor community: if investors suddenly resumed financial support for producers, funding their capital expenditures with new funds, it would have been terminal for People, Ideas & Objects. We, along with our user community and their service provider organization, would have failed spectacularly due to a distinct lack of credibility and support in the short term. We would have seen such an action as a betrayal by investors toward the future of the oil and gas industry and all those who expect and depend on a turnaround. If the industry's spendthrift leadership in the form of officers and directors regained their investors' trust, faith, and goodwill, People, Ideas & Objects would be set back significantly in terms of our product horizons.

Therefore, to keep the overall opportunity open, we had to be patient until we saw what investors would do. We kept our powder dry and our candles lit until we knew where we were headed. Now, we have that clarity. We would not risk our user community's careers, nor waste their time or money, by associating them with us and potentially subjecting them to the producers' vilification. We have a viable business model, a plan, and a vision to address the industry's current issues. We indirectly have the support of oil and gas investors who have not supported producer officers and directors since 2015. These investors have tried to deal with dysfunctional leadership and are now abandoning them due to their inaction. I see investors' actions as terminal to producer firms' leadership. There is no stronger message that theirs is a flawed and failed corporation than having their investors give up on them.

Commissions

I am pleased to announce that People, Ideas & Objects are instituting a Sales Commission Program for our Preliminary Specification, targeting North American-based producer firms. This program is open to individuals within or outside the oil and gas industry who believe they can close the sale of an ERP software development, as defined in the Preliminary Specification, to North American producers. This includes direct sales to producer firms, investor groups seeking attractive licensing opportunities in oil and gas production and technology, or others interested in participating in our Profitable Production Rights.

Now is the time to offer this opportunity. Our perspective on the industry is well-documented in our writings. Our vision, plans, and Preliminary Specification resonate with those within the industry. What officers and directors dismissed as “opportunity costs'' over the past decades has materialized into a substantial value proposition, irretrievably lost due to their inaction. Our concern for the industry's future if these issues remain unaddressed is severe, with significant detrimental effects on the oil and gas economy. This turning point calls for changes, such as those defined in our Cloud Administration & Accounting for Oil & Gas software and services. This service, funded by Profitable Production Rights proceeds, will control producer access. Chronic inaction and destruction by producer officers and directors necessitate others taking steps to resolve these industry difficulties. The first step is to organize ourselves to tackle these issues effectively. In the 21st century, a software system that defines, supports, but also constrains an organization needs to be built. Organizing North American producers toward a dynamic, innovative, accountable, and profitable outcome will not occur otherwise.

We are at a point where sales must begin, and our budget needs funding. Our pricing is based on our value proposition. We assert that implementing the Preliminary Specification will generate $25.7 to $45.7 trillion in incremental revenue and profitability for the greater oil and gas economy over the next 25 years. Our Intellectual Property provides substantial and proven value, as evidenced in the North American natural gas market over the past year, and is exclusive to the Preliminary Specification business model. Decades of evidence show that producer officers and directors are unable to resolve these issues. Producer firms have chosen to do nothing, and others will now take it from here.

The commission for closing a sale is 15% of the sales price to the producer. Producer costs are based on the North American sourced production assessment per barrel, plus commission. The per barrel assessment is $1,000/boe, including commission is $1,150/boe. People, Ideas & Objects pricing is based on the value proposition we bring to the market. Without the Preliminary Specification, the industry is engaged in wasteful pursuits and lacks plans or vision for the future. Sales commissions are paid upon closing.

The sales process may be long and complicated, incurring costs that are the responsibility of the individuals participating in this commission program. People, Ideas & Objects will support the process to the extent of our ability. Unlike our Whistleblower Program, there is no exclusivity granted to any individual. However, for a fee of $5,000 USD, individuals can buy a two-year exclusive license to sell to a specific producer. License renewals are granted but will lose the exclusivity of the initial license.

For startups and small oil and gas producers, two classifications dedicated to People, Ideas & Objects et al Cloud Administration & Accounting for Oil & Gas software and services, we do not expect initial sales interest. It is likely they will join on their own or towards the end. The Preliminary Specification provides enhanced and distinct benefits over other producer firm classifications. Their participation will not be material to this Sales Commission Program unless an individual expresses otherwise, possibly as an allocation for startups or small producer firms with an aggregate production profile of X boe/day representing a number of producers.

Driven by a strong sense of urgency, I have seen exponential growth in the market's sense of urgency. Therefore, I am announcing our "First to Close Bonus" on these Sales Commissions. A "First to Close Bonus" of 2x commission will be paid to whomever secures the first sale. This bonus will be paid from People, Ideas & Objects sales proceeds.

Conclusion

User community-defined ERP software developments, such as People, Ideas & Objects' Preliminary Specification, are the only effective methods to generate quality ERP systems. Asking developers, trained in their specific disciplines, to write software for oil and gas accounting and administration on the broad scope and scale of the Preliminary Specification is impossible without direct user involvement. However, user involvement significantly escalates the budget for ERP development and implementation, often making it the first budget item to be cut. Given the scope, scale, and necessity of resolving issues in the oil and gas market, we cannot afford to make such cuts. Our proven value proposition, understood by all in the industry, renders discussions about our budget moot. The industry wastes the value of our budget every month.

There are substantial conflicts and contradictions in seeking funds from existing producers to rebuild the industry. One perspective is that we are indirectly assessing a royalty or fee on oil and gas production through the Profitable Production Right license. Each barrel of oil equivalent (boe) per day will need to secure this license to be processed through our Cloud Administration & Accounting for Oil & Gas software and service. This indirect cost on profitable production is appropriate for fostering a dynamic, innovative, accountable, and profitable industry.

I see an obligation on behalf of those officers and directors who have willingly destroyed the industry to support this initiative. Doing the right thing would mitigate their personal risk in terms of maintaining their Officers and Directors Liability Insurance, a risk they do not share with us. They seem uninterested in addressing the fact that their investors have acted in ways demanding action. Alternatives in the market have identified and resolved the issues, but these officers and directors falsely refuted those alternatives, flipped in and out of the oil and gas and shale industries, and remain indifferent to the tragic losses and damages they’ve caused.

The reality we face is that, after decades of dealing with this difficulty, the details of how these communities are financially supported remain unclear to me otherwise. Profitable Production Rights licenses assess a fee on oil and gas production for the use of our Cloud Administration & Accounting for Oil & Gas software and service. This will be the only method through which North American oil and gas producers can produce profitably. Otherwise, they must explain to any interested parties why they are not.